Get to know the basics of workers comp insurance.

Basic work comp requirements.

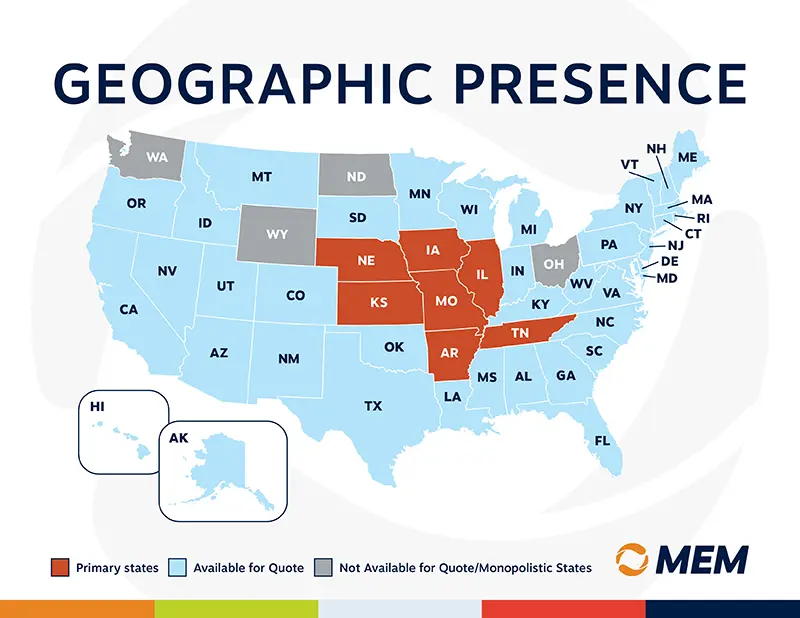

MEM has been the Missouri work comp leader for 30 years. We now provide coverage throughout the Midwest. Wherever you have exposures, we’ve got you covered — multistate coverage is available nationwide.

Looking for more information about how your premiums are calculated? Check out this infographic or learn more about how the calculation breaks down on our blog.

How work comp premiums are calculated.

Your work comp policy’s premium with MEM is determined by your:

How to reduce your work comp premiums.

It sounds deceptively simple, but the best way to reduce your premium is to avoid injuries. At MEM, that’s where we excel, helping you build a safety-focused culture. It’s an approach that pays in more ways than one. When people are safe at work, they’re happier and more productive. Reducing or eliminating work comp claims lowers your premium over time. And if an injury does occur, managing the claim process can also keep premium costs down.

Work Comp Basics FAQ

How to purchase insurance from MEM.

It’s easy. Simply talk to your independent insurance agent and tell them you’d like to choose MEM as your workers compensation carrier. If you don’t have an agent, we’ll help you find one.